Accidents rarely announce themselves. They happen suddenly, often without warning, and can change lives in a matter of seconds. Whether it is a road collision, a workplace incident, a slip and fall, or an unexpected injury during daily activities, the aftermath of an accident can be overwhelming—physically, emotionally, and financially.

This is where accident insurance claims come into play. Understanding how personal injury insurance works, how to file a claim, and how to protect your rights can make a critical difference in recovery and long-term stability.

This article offers in-depth, practical insights into accident insurance claims and personal injury coverage—written for individuals, professionals, and decision-makers who want clarity, confidence, and control when it matters most.

Understanding Accident Insurance and Personal Injury Coverage

Accident insurance is designed to provide financial protection when injuries occur due to unexpected events. Unlike general health insurance, accident insurance focuses specifically on injuries caused by sudden and accidental incidents.

Personal injury coverage typically includes compensation for:

- Medical expenses

- Hospitalization and surgery

- Rehabilitation and therapy

- Lost income due to inability to work

- Permanent disability or disfigurement

- In severe cases, death benefits

The goal is not just treatment—but financial continuity.

Why Accident Insurance Claims Matter More Than Ever

In today’s fast-paced world, risks are everywhere. Increased mobility, urban congestion, demanding work environments, and active lifestyles mean accidents are more common than many realize.

Without proper accident insurance:

- Medical bills can escalate rapidly

- Recovery time can cause income loss

- Families may face unexpected financial strain

An effective insurance claim acts as a financial shock absorber, helping individuals recover without long-term damage to their personal or professional lives.

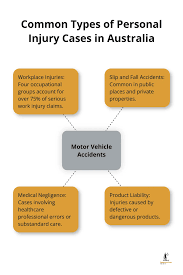

Common Types of Personal Injury Accidents

Understanding the most common accident scenarios helps policyholders anticipate coverage needs.

Road Traffic Accidents

Car, motorcycle, bicycle, and pedestrian accidents are among the most frequent causes of personal injury claims. These incidents often involve:

- Fractures and spinal injuries

- Head trauma

- Long-term rehabilitation

Workplace Accidents

Industries such as construction, manufacturing, logistics, and healthcare carry higher injury risks, including:

- Falls from height

- Machinery-related injuries

- Repetitive strain injuries

Slip, Trip, and Fall Incidents

These can occur in public spaces, offices, or private properties and often result in:

- Broken bones

- Soft tissue injuries

- Head injuries

Sports and Recreational Accidents

From gym injuries to extreme sports, physical activities can lead to claims if properly insured.

The Anatomy of an Accident Insurance Claim

Filing an accident insurance claim is a structured process. Knowing the steps reduces delays and increases the chance of successful compensation.

Step 1: Immediate Medical Attention

Always seek medical treatment first. Insurance providers require medical documentation to validate claims.

Step 2: Incident Documentation

Details matter. Record:

- Date and time of the accident

- Location

- Circumstances

- Witness statements if available

Step 3: Notify the Insurance Provider

Most policies require notification within a specific timeframe. Delays can jeopardize claims.

Step 4: Submit Required Documents

Common documents include:

- Medical reports

- Hospital bills

- Accident reports

- Proof of identity

- Claim forms

Step 5: Claim Assessment and Settlement

The insurer reviews the claim, verifies coverage, and determines compensation.

Key Factors That Influence Claim Approval

Not all claims are approved automatically. Several factors influence outcomes.

Policy Coverage and Exclusions

Every policy has limits and exclusions. Understanding them upfront prevents disappointment later.

Timeliness

Late reporting is one of the most common reasons claims are delayed or denied.

Accuracy of Information

Inconsistent or incomplete information raises red flags during assessment.

Medical Evidence

Clear medical documentation linking injury to the accident is essential.

Common Challenges in Accident Insurance Claims

Despite having valid coverage, many claimants face obstacles.

Claim Delays

Missing documents, unclear medical reports, or verification issues can slow processing.

Partial Settlements

Insurers may approve claims but reduce payouts based on policy limits or exclusions.

Claim Rejection

Claims may be denied due to:

- Policy exclusions

- Non-disclosure of pre-existing conditions

- Late reporting

Understanding these risks helps policyholders prepare better.

Personal Injury Compensation: What Can Be Claimed?

Accident insurance claims may cover a wide range of costs.

Medical Expenses

Including:

- Emergency care

- Hospital stays

- Surgery

- Medication

- Follow-up treatment

Loss of Income

If injuries prevent work, insurance may compensate for lost wages during recovery.

Rehabilitation Costs

Physiotherapy, occupational therapy, and psychological support are often included.

Permanent Disability Benefits

If injuries result in long-term impairment, compensation reflects the severity and impact on earning capacity.

Accidental Death Benefits

In fatal cases, benefits are paid to designated beneficiaries.

The Role of Medical Reports in Personal Injury Claims

Medical documentation is the backbone of any accident insurance claim.

High-quality medical reports should:

- Clearly diagnose injuries

- Link injuries directly to the accident

- Outline treatment plans and recovery timelines

- Assess long-term impact

Incomplete or vague reports weaken claims significantly.

Personal Injury Claims and Mental Health

Not all injuries are visible. Accidents can leave lasting psychological effects such as:

- Anxiety

- Depression

- Post-traumatic stress disorder (PTSD)

Modern insurance policies increasingly recognize mental health as a legitimate component of personal injury claims, provided it is medically diagnosed and documented.

Accident Insurance for Professionals and Executives

From a leadership perspective, accident insurance is more than personal protection—it is strategic risk management.

Executives, entrepreneurs, and high-level professionals often face:

- High income dependency

- Business continuity risks

- Reputation exposure

An untreated injury or prolonged recovery without coverage can disrupt operations and decision-making.

For companies, offering accident insurance:

- Enhances employee security

- Reduces downtime

- Strengthens employer branding

Digital Claims: The Evolution of Insurance Processing

Technology has transformed how accident insurance claims are handled.

Modern insurers offer:

- Online claim submission

- Digital document uploads

- Mobile claim tracking

- Faster settlements

This improves transparency and reduces administrative stress for claimants.

How to Strengthen Your Accident Insurance Claim

Preparation makes a difference.

Know Your Policy

Read coverage terms before accidents happen—not after.

Keep Records Organized

Maintain copies of:

- Medical bills

- Reports

- Communication with insurers

Be Honest and Detailed

Transparency builds credibility and trust during assessment.

Follow Medical Advice

Non-compliance with treatment plans can weaken claims.

Legal Considerations in Personal Injury Claims

In some cases, accident insurance claims overlap with legal liability claims, especially when negligence is involved.

Understanding the difference:

- Insurance claims focus on policy benefits

- Legal claims pursue compensation from responsible parties

Both can coexist but require careful coordination.

The Cost of Not Having Accident Insurance

The absence of coverage can be financially devastating.

Potential consequences include:

- Medical debt

- Loss of income

- Depleted savings

- Long-term financial insecurity

From a cost-benefit perspective, accident insurance is one of the most efficient risk-transfer tools available.

Accident Insurance Myths That Need to Go

“I’m Healthy, I Don’t Need It”

Accidents are unrelated to fitness levels.

“Health Insurance Is Enough”

Health insurance may not cover income loss or disability benefits.

“Claims Are Too Complicated”

With proper documentation, most claims are manageable.

The Future of Personal Injury Insurance

The insurance industry is evolving rapidly.

Emerging trends include:

- AI-assisted claim assessment

- Faster settlements

- More inclusive mental health coverage

- Personalized insurance plans

These developments aim to make claims more human-centric and efficient.

Final Thoughts: Protection That Pays When It Matters

Accidents are unpredictable, but the financial impact doesn’t have to be.

Accident insurance claims represent more than paperwork—they represent security, dignity, and recovery. When handled correctly, personal injury insurance allows individuals and families to focus on healing instead of financial survival.

Whether you are an individual protecting your livelihood, a professional managing risk, or a business leader safeguarding people and continuity, accident insurance is not optional—it is essential.

Preparation today ensures resilience tomorrow.

Word Count:

889

Summary:

There�s nothing that has a greater impact on evaluating a personal injury insurance claim than the damage done to your body, the medical bills that are a direct result of that injury and the �pain and suffering� you were forced to deal with.

Keywords:

Car Inurance, Car, Inusrance, Finance, Business

Article Body:

Besides botching up your body (and sometimes your love life) what else does the injury mean to you? It means a ton of financial expense�s, including repairing your motor vehicle, lost wages, a shock to your life style, a tremendous inconvenience and short or long periods of pain and discomfort – – all of it a direct result of your injuries.

Plus, there’s a long list of possible medical expenses. For example: Doctor/Chiropractor, Prescription Drug Bills, Ambulance, Emergency Room Care, Hospital or Clinic, Specialist and/or Dentist, Laboratory Fees and Services, Diagnostic Tests, X-Rays and (CT) Scan, Prosthetic Appliances or Surgical Apparatus (Canes & Crutches), Physical Therapy, Registered and/or Practical Nurse Fees, Gauze and Tape, Ace Bandages all of which the insurance company must pay whether they like it or not!

Also, Creams, Lotions, Ointments, Balms and Salves, etc. (Should the lady in your life apply any of these to your aching body I’m sorry to tell you this but her labor is not an expense you can claim).

YOU MUST BE COMPENSATED BY THE INSURANCE COMPANY FOR ALL OF THE ABOVE: It’s true that a very small percentage of motor vehicle accidents cause big, serious injuries but that doesn’t mean you shouldn’t be paid big, serious bucks!

EXAMINATION BY THE INSURANCE COMPANY DOCTOR: Claims Adjuster Henry Hard-Nose of Rock Solid Insurance will usually try to pull a fast one insisting he wants you to be examined by the physician of his choice, the local medical con-man of all time, Dr. Nuttin’ Wrong. Beware of such a request. Doctors assigned by the insurance company are notorious for stating, in the report they’re paid big bucks to execute, “There is no objective basis”, for your complaints.

You don’t have to agree to be examined by Dr. Nuttin’ Wrong. Rock Solid Insurance cannot insist that you submit to their doctor for an examination unless your claim actually becomes a formal court case. So, hold your ground until your attending physician, Ole �Doc� Comfort, has released you. After that it’s okay to agree to be examined because by then it’s too late! So much time will have passed it will be impossible for Dr. Wrong to minimize the pain, discomfort and suffering your injury has caused you.

WHAT TO DO ABOUT YOUR MEDICAL BILLS IF YOU MAKE THE MISTAKE OF OBTAINING LEGAL HELP FROM ATTORNEY I. M. SHARP: Should yours be a case in which there’s no question that you’re not at fault, make it clear to the Legal Beagle you’ve hired, I. M. Sharp, Esquire, that you expect his Contingency Fee will not apply to that which he recovers for the damage to your car, your medical bills, and/or your payment for lost wages. You tell him these are damages you would have collected ANYWAY – – whether he was handling the case for you or if you settled it yourself. Don’t you dare be foolish enough to hand him a huge percentage of that which you were going to be paid by the insurance company, whether Attorney Sharp handled the case or not. To do so is the height of financial stupidity!

YOUR BODILY INJURIES: It’s a proven fact that the vast majority of motor vehicle accidents cause minor injuries. While bodily injury pain can be specifically measured the limits of what you can endure cannot. Each of us has a different “pain threshold” – – that is, the point at which we begin to feel physical pain. The amount and quality of pain you feel is not strictly dependent on the bodily injury inflicted. It has a lot to do with your previous experience, how well you remember it, and your ability to understand what caused you that pain, and its consequences, the last time around.

Stress and strain magnify physical pain plus personal anxiety will greatly increase it. There are also emotional reactions to the injury. A bodily injury is bound to cause some degree of mental distress. The duration and severity that depends on a number of factors: The type of individual you are, the ultimate consequences of the injury you sustained, and the life stresses or strengths you’re experiencing at the time of your injury. (If you can’t stand her and she takes a powder you�ll handle your pain better if you really dig the chick and she dumped you for your best friend)!

When it comes to muscle injuries one thing you must keep in mind is that when one part of the body demands rest (by sending out a pain signal) and – – without your even realizing it – – you help your body by placing a new burden on other muscles. It gets complicated because although those muscles may not have been directly injured in the accident, they can still get buggered up and produce a lot of pain because of their new role.

DISCLAIMER: The only purpose of this claim tip is to help people understand the motor vehicle motor vehicle accident claim process. Neither Dan Baldyga nor (name the magazine/newsletter and/or web site) make any guarantee of any kind whatsoever; NOR do they purport to engage in rendering any professional or legal service, NOR to substitute for a lawyer, an insurance adjuster, or claims consultant, or the like. Where such professional help is desired it is the INDIVIDUAL�S RESPONSIBILITY to obtain said services.

Tinggalkan Balasan